When looking into what differentiates the rich from the poor, I’ve begun to notice a pattern of habits. These habits have been shared by a variety of millionaires themselves so one cannot help but consider the importance of adopting them yourself. It worked for them and they swear by it. After all, you’d be confident in following the diet and workout routine of someone who has your ideal figure.

When looking into what differentiates the rich from the poor, I’ve begun to notice a pattern of habits. These habits have been shared by a variety of millionaires themselves so one cannot help but consider the importance of adopting them yourself. It worked for them and they swear by it. After all, you’d be confident in following the diet and workout routine of someone who has your ideal figure.

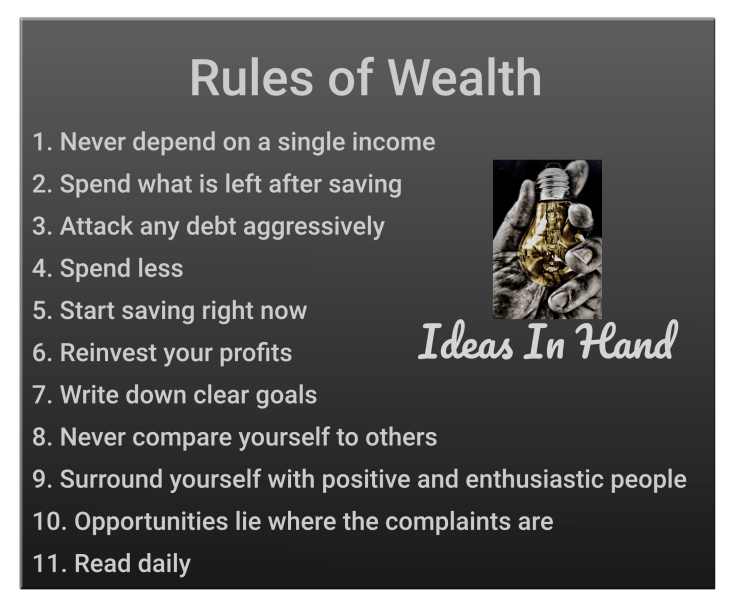

In no particular order other than 1-6 being money orientated and 7-11 being about your person:

Rule Number 1 – Never depend on a single income

I suspect that this rule has been idealised by people all over the world, regardless of their actual financial status. It is suggested that there are mainly 7 potential sources of income that people should look to utilise. Click here to see the 7 Sources of Income. I can’t help but feel if you had a dabble in each of the 7 simultaneously you would probably lose track of what’s what, I know I would. I would recommend you do your own research to identify what works for you and spend time getting comfortable and confident in one before moving onto another.

Rule Number 2 – Spend What Is Left After Saving

Otherwise referred to as “Pay Yourself First”, this rule is one of the easiest one you can implement immediately. How often do you feel like you get to the end of each month and have no money left? You probably had a good couple of weekends with friends and treat yourself to some new clothes or the latest tech, but how much money did you actually put aside to invest or save for a rainy day or emergency? As soon as you receive your pay check for the month you should always put some of it away and preferably out of site to reduce temptation of dipping into it. It is recommended you set aside around 20% of your wages for savings and investment. If you do this at the start of the month you will find it easier to budget around this for the rest of the month. This leads nicely onto the next 2 rules

Rule Number 3 – Attack Any Dept Aggressively

Dept is an unusual topic to work out. Some debt seems to be good, but mostly it is seen as bad. I would say a great example of this would be your mortgage, often quoted as being one of the cheapest loans you will ever get. Without this debt, you would likely not be able to afford to buy a house. If you can afford to buy a house without a mortgage, this website probably isn’t for you. Once you own the house there is a high chance that over time, the estimated value of your property will increase and the more you pay off your mortgage the cheaper the interest becomes. Essentially, it’s a debt that can earn you money (assuming the interest earned is lesser than the annual increase in property value). In this example, the ambition would be to own your house outright having paid off the mortgage and the property continue to increase in value over time. The quicker you can pay off your mortgage, the less interest you will pay overall and the less susceptible you will be to fluctuations in interest. Check out Money Saving Experts Mortgage Overpayments Calculator to see what the overall impact would be if you attacked your outstanding mortgage aggressively.

Rule Number 4 – Spend Less

Learn to live within your means. Even if you have done the right thing and put money aside at the start of the month, you should still remain conscientious as to what you are spending between now and your next payday. I am not by any means saying spend as little as possible and becoming a social recluse, it’s bad for your health. What I believe this rule is attaining to is simply be considerate of where your money goes and monitor your spending habits. Before you buy something, ask yourself questions like, do I actually need this or are there cheaper alternatives? This is after the biological needs for human survival; as depicted in Maslow’s Hierarchy of needs, are met (i.e. food, water, sleep, shelter, sex). If this first step in the hierarchy is not met, your body will not be able to perform optimally.

Rule Number 5 – Start Saving Right Now

Just like that diet you’ll start on Monday or the DIY you will definitely do this weekend, saving is an activity that is best started immediately. I mean like right now. Another one from Money Saving Expert, check out his page on Top Savings Accounts; which gets updated daily, and find which one is right for you. No, you are not going to become a millionaire in the next 5 years just by putting the minimum amount in and leaving it to compound for the next 5 years, it doesn’t work like that. Especially as interest rates are so low at the moment. All of the articles or posters you’ve seen that depict a figurative 10% interest rate that compounds over x number of years are complete tosh. The best interest rates in the UK at the moment are no higher than around 2.7% (As of April 2019). The point of this rule is to get you in the mindset of just doing it and to get consistent at it, no excuses, and the best time for this to start is right now.

Rule Number 6 – Reinvest Your Profits

You need to make your money work for you. In the early days of you following these rules and changing your mindset, the profit margins are unlikely to be considerable. You’re going to have to be patient (one of my own personal biggest issues). By reinvesting your profits, you will begin to create what is called the Snowball Effect where your earned interest will begin earning interest. The same effect is seen when paying off multiple debts. As debt gets closed, you can take the money that was paying that debt and add it to the repayments of other debts. Bear in mind the snowball effect can also be a bad thing if debt grows in interest. If left to grow, you will get to the point where your initial loan has been paid back but all your left paying is the interest gained.

Reinvesting your profits is not all about putting back into savings accounts. For example, if you begin making good money from your savings and other sources of income you could look to reinvest your earnings into property or stocks and shares etc. The main focus here is to keep using your newly earned money to earn you more money.

Rule Number 7 – Write Down Clear Goals

Having a clearly defined set of goals will help you stay on your path to success. After all, you do kind of need to know where you are going in order to have a path. Knowing where you actually want to be is incredibly important, so make sure you give it some deep thought. Once you’ve worked it out, write it down, memorise it, and live it. Make it an integral part of your daily routine and decision-making process. If your goal is quite an ambitious one, break it down into stages, and keep breaking it down until you have a list of achievable tasks. Ideally you could now give each of these tasks a date for completion which will turn you goals into a plan which you can use to track your progress.

The critical part of this rule is to understand why you want to do this in the first place. What is your real motivation behind it? Simon Sinek, a best-selling author and leadership expert, took the world by storm in 2009 for his TED talk on “Start with Why – How Great Leaders Inspire Action.” Within the talk, and his book Start with Why, he refers to his concept of the Golden Circle. The diagram he depicts is made up of 3 concentric circles with WHY at the centre, HOW in the middle, and WHAT in the outer. He proceeds to explain that:

“Every single person on the planet knows WHAT they do. Some know HOW they do it. Very few people or organisations know WHY they do what they do. The inspired leaders and the inspired organisations, regardless of their size or industry, all think, act and communicate from the inside out.”

Rule Number 8 – Never Compare Yourself to Others

A rule that is easier said than done, I think we all end up getting a little jealous; whether you care to admit it or not, of other people who seem to be better off, have more friends, do more exciting things, or always seem to be on holiday etc. and this is only fuelled by social media. As Steven Furtick, Lead Pastor of the Elevation Church and best-selling author, said:

“The reason we struggle with insecurity is because we compare our behind-the-scenes with everyone else’s highlight reel.”

This ultimately becomes important if you find yourself comparing where you are just starting out, with where; for example, the Forbes list of the Richest People in the World are now. I picked this list as an extreme to make a point that what you see from peoples highlight reels is not always been handed to them on a platter. Yes, they are genuinely incredibly wealthy now but let’s take a look at where some of them came from.

Jeff Bezos. Founded Amazon out of his garage in Seattle in 1994 with the intention of selling books online. He is now worth over $131 Billion

Mark Zuckerberg founded Facebook in 2004 from his dorm room as a way of connecting people around his university. He is now worth over $62 Billion.

Jack Ma founded Alibaba.com from his apartment in April 1999 with a goal to help export Chinese products to the global market. He is now worth over $39 Billion

Phil Knight founded Nike Inc. in 1971 after successfully selling running shoes from the boot of his car at track meets in America. He is now worth over $33 Billion.

It’s one thing to be born into wealth and be able to continue the legacy which is still very impressive, but I have a whole different level of respect for the people who can believe in an idea, even in its early infancy, and work hard to make it a success. This rule is essentially emphasising the whole don’t judge a book by it’s cover idiom. There are a number of highly successful people that have worked incredibly hard to become what they are today. Don’t envy these people, look up to them. This leads us nicely to the next rule.

Rule Number 9 – Surround Yourself with Positive and Enthusiastic People

How often have you heard the phrase “It’s not what you know, it’s who you know?” Wealthy people are just great at networking. Period. You can’t possibly know everything, but the wider the range of people you keep around you the more likely you are to get sound advice or pick up on useful information. Two quotes that stand out for me on this subject are:

“If you’re the smartest person in the room, you are in the wrong room.”

And

“You are the average of the 5 people you spend the most time with”

Essentially, the best way for you to improve is to surround yourself with people who are most likely to support you in what you do and have a personality that resonates most with the person you aspire to be. Generally, these are going to be likeminded people who have similar aspirations. If you surround yourself with pessimistic and negative people, they will bring you down and convince you that your ideas are stupid or you can’t do it so why bother.

Rule Number 10 – Opportunities Lie Where the Complaints Are

People seem to enjoy a good moan and they love to complain. The benefit to this is that occasionally there is a diamond in the rough. How many products and services that have ever been created do you think came about because someone moaned about how difficult or boring something was or because it took too long or it doesn’t work very well. Listen out for these as you go about your day and think to yourself “can this be done better?” There is always room for improvement, you just have to spot it.

Rule Number 11 – Read Daily

If you don’t already do so, getting into the habit of reading on a regular basis will have a massive impact on your personal growth. Wealthy people are often quoted about how much and how often they read.

Bill Gates – 50 books per year

Warren Buffet – 5 to 6 hours per day or around 500 pages

Oprah Winfrey – Quoted books were “her pass to personal freedom”

Elon Musk – Quoted he “learnt to build rockets simply from reading books”

David Rubenstein – 6 books per week

Mark Cuban – 3 hours per day

You get the picture. Let’s be honest, these people aren’t usually known for sitting around twiddling their thumbs so if they can find time to read, so can you. Reading is not just for personal entertainment. It’s okay to unwind with a good book which tickles your imagination but you should be reading a higher percentage of nonfiction. Jim Rohn once said “Formal education will make you a living; self-education will make you a fortune.” Nonfiction books are an author’s way of providing you with a best bits summary of the last few decades of their education and experiences.